Collect requests are gone. A payment page is the better replacement.

Instead of chasing people with requests, share your WithUPI link and let them pay on their own terms - faster, with less friction.

If you used to open your UPI app, tap Request money, enter someone's UPI ID, and wait for them to approve the request, that flow may not work the way it used to.

From October 1, 2025, person-to-person UPI collect requests were discontinued. In simple terms, one individual can no longer send another individual a UPI request that the other person accepts by entering their UPI PIN.

This does not mean UPI payments are gone. It also does not mean people cannot pay you.

It means the payment flow has shifted more clearly toward payer-initiated payments: the person who is paying should open their UPI app, scan your QR, tap your UPI link, or enter your UPI ID themselves.

For freelancers, creators, tutors, consultants, and small businesses, the change is a good reason to clean up how you ask for money.

Image source:

Unsplash, photo by Markus Winkler

Quick answer

If UPI request money is not working for a person-to-person payment, do this instead:

- share your UPI QR code

- share a direct UPI payment link

- share your UPI ID with the exact name the payer should see

- send a short payment message with the amount and reason

- use one clean payment page instead of sending different details every time

- use WithUPI Requests for direct asks and group splits

The goal is simple: make it easy for the payer to start the payment confidently from their side.

What was a UPI collect request?

A UPI collect request was a "request money" flow.

Instead of the payer starting the payment, the receiver could initiate a request. The payer would see a prompt inside their UPI app, review the amount, and approve it with their UPI PIN.

It was useful for situations like:

- splitting a dinner bill

- asking a friend to repay money

- collecting rent from a flatmate

- requesting a project payment from a client

- reminding someone about a pending small amount

The feature reduced typing for the payer. But it also created a risk: a payment approval prompt could arrive from someone else, and a confused user might approve it without fully understanding that money would leave their account.

That is why collect requests became sensitive.

What changed from October 1, 2025?

From October 1, 2025, banks, payment service providers, and UPI apps stopped initiating, routing, or processing person-to-person collect transactions. NPCI's circular on this is titled Discontinuing the service of UPI Collect Request for Person to Person (P2P) transactions.

The important phrase is person-to-person.

This change is about one individual sending another individual a UPI collect request. Normal UPI payments still work. QR codes still work. UPI IDs still work. UPI links still work. Merchant checkout flows may have their own rules depending on the payment provider and transaction type.

So if you are trying to get paid by a client, student, friend, or family member, the practical answer is not "UPI is broken."

The answer is: ask them to pay you directly.

Why was this feature removed?

The main reason was fraud prevention.

Collect requests could be misused because they put a payment approval prompt in front of the payer. A scammer could call or message someone, create urgency, and ask them to approve a request that actually debits money from their bank account.

For people who understand UPI well, that sounds obvious. For many users, especially when they are distracted or pressured, it is not always obvious enough.

Payer-initiated payments are easier to reason about:

- the payer chooses to scan, tap, or enter the UPI ID

- the payer sees the payee name before entering the PIN

- the payer controls when the payment starts

- the payer is less likely to mistake a debit request for incoming money

This does not remove every possible UPI scam. It just closes one pathway that was easy to misuse.

What should freelancers and small businesses do now?

If your old habit was "I will send you a UPI request," switch to "Here is the payment link."

That small wording change matters.

The person paying you should be able to see:

- who they are paying

- how much they need to pay

- what the payment is for

- which UPI name they should expect in the app

- whether they can use any UPI app

That is more professional than sending a raw UPI ID and then adding three follow-up messages.

Option 1: Share a UPI QR code

A QR code is still the most familiar UPI payment method in India.

It works well when:

- the payer is nearby

- you are collecting after a class, session, or delivery

- you are showing the code on another screen

- you want the payer to scan with any UPI app

The weakness is that QR screenshots can become messy over time. People crop them, forward old versions, or save them without context. If your display name, UPI ID, or business name changes, old QR screenshots can keep floating around.

Use a QR code, but make sure the payer also knows the name they should see before entering their PIN.

Option 2: Share a UPI payment link

A UPI payment link is useful when you are talking to someone on WhatsApp, Instagram, email, or chat.

Instead of asking them to copy a UPI ID, you can send a link that opens their UPI app and prepares the payment.

This works especially well for:

- freelance invoices

- coaching fees

- design or development advances

- consultation payments

- content, workshop, or event payments

- recurring small client payments

The key is to add context around the link. Do not send only the link with no explanation.

Option 3: Share a clean payment page

This is usually the best option if you accept payments from people who do not know you well.

A payment page can show:

- your name or brand

- your UPI ID

- your QR code

- a payment button

- basic context about who the payment is for

- one reusable link you can put in invoices, bios, emails, and messages

That makes the payment feel less random.

It also reduces the number of times you need to explain the same thing:

- "This is my UPI ID."

- "Yes, that name is correct."

- "Use this QR instead."

- "Send me the screenshot after paying."

- "No, that older QR is not the one I use now."

For a client, those messages are friction. For you, they are admin work.

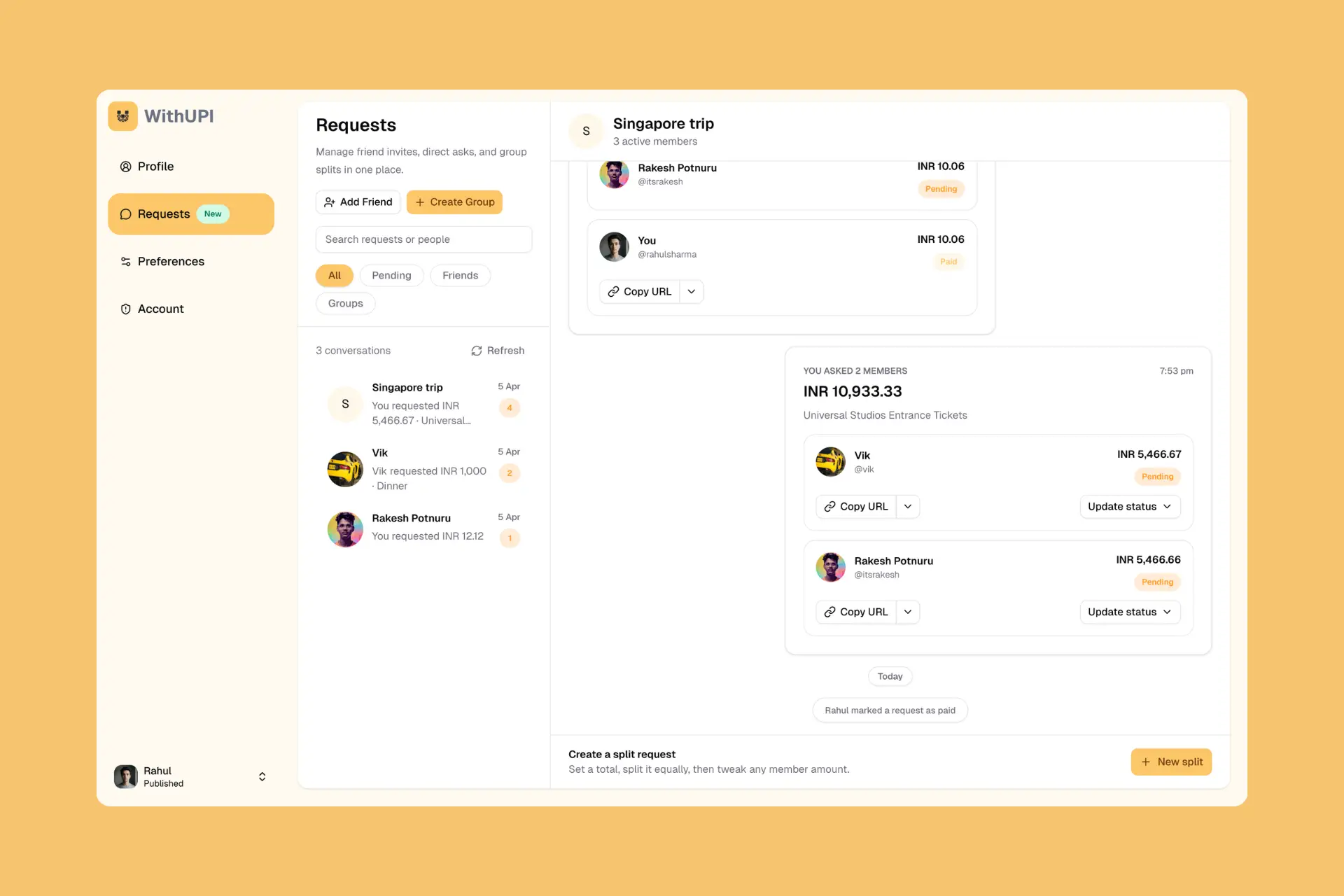

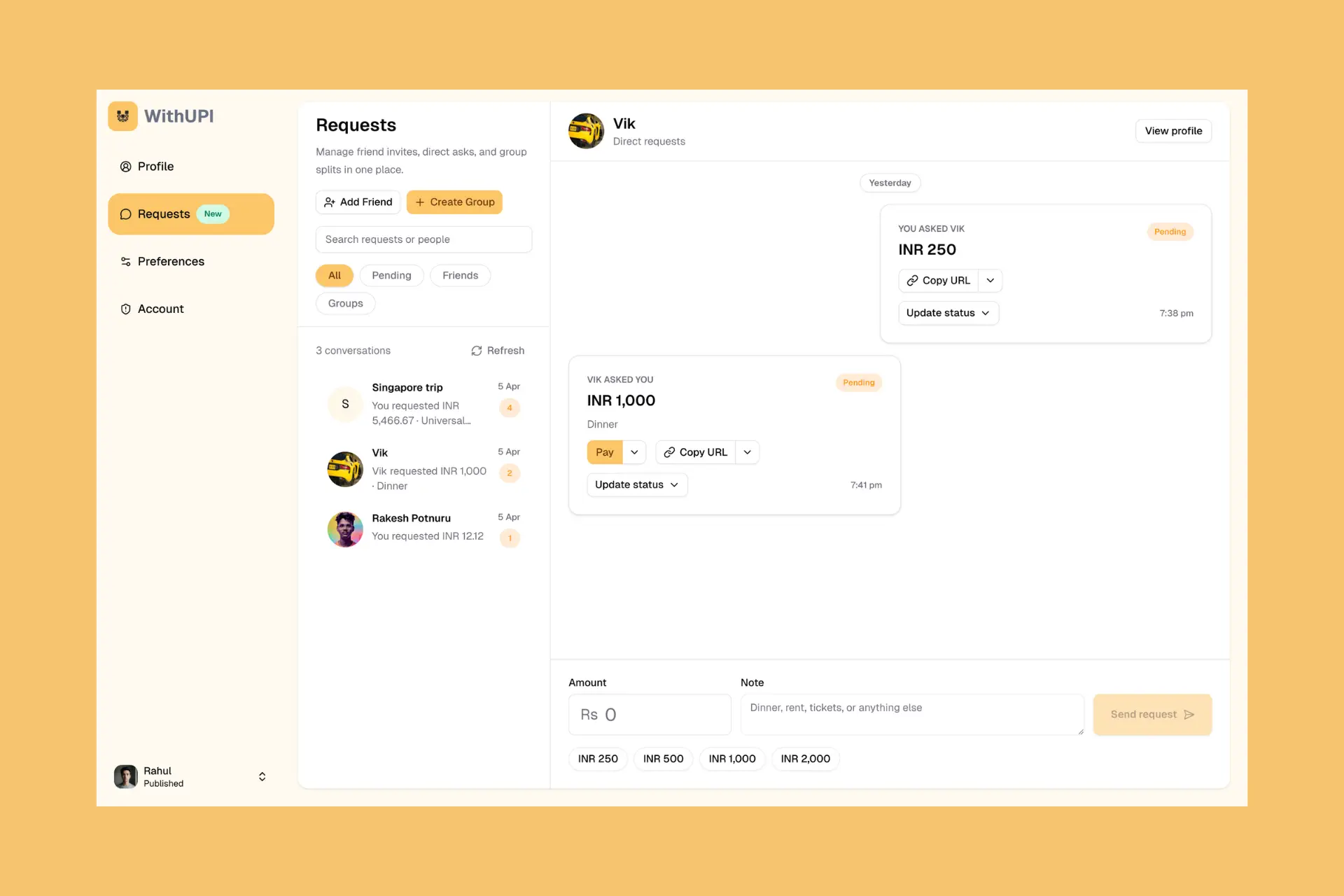

Option 4: Use WithUPI Requests

If you want something closer to the old "request money" habit, use WithUPI Requests.

WithUPI Requests is different from the discontinued UPI collect request flow. It does not push a debit approval prompt into someone's banking app. Instead, it gives you a cleaner workspace for asking, tracking, and paying through a payer-initiated UPI flow.

You can use it to:

- send a direct request to one person with an amount and note

- split one total across a group

- keep incoming and outgoing requests in one inbox

- give the payer a clear

Payaction - show a QR when scanning is easier

- keep request status visible after payment

That makes it useful for real-world situations where the payment itself is simple, but the coordination is not.

For example:

- a tutor collecting monthly fees from a student

- a freelancer asking for an advance from a client

- a friend splitting a shared cab or dinner bill

- a small team collecting for a shared expense

The important difference is control. The payer still starts the UPI payment themselves. WithUPI just keeps the request, amount, note, pay action, and status in one place so the conversation does not scatter across chats and screenshots.

What not to do

Avoid these habits:

- do not send multiple UPI IDs unless there is a clear reason

- do not send an old QR screenshot without checking it

- do not assume the payer knows which name should appear

- do not ask someone to approve a request if their app no longer supports it

- do not make payment instructions longer than the actual invoice

People are already careful around payments. Confusing instructions make them more careful, not faster.

Does this affect split bills and group payments?

It can, depending on how the app implemented the split.

If the split relied on person-to-person UPI collect requests, that old approval flow may no longer work. Apps may replace it with reminders, payment links, QR flows, or other app-specific experiences.

For casual groups, the easiest fallback is still simple:

- share the amount each person owes

- share one UPI link or QR

- ask each person to pay directly

- track who has paid

For business payments, do not run your collection process like a group chat. Use a clear payment destination and keep the message professional.

Does this mean clients can refuse to pay more easily?

Not really.

A collect request never guaranteed payment. The payer still had to approve it.

The bigger issue is clarity. When you remove the in-app request prompt, your external payment request needs to carry more of the load.

That means your payment ask should include:

- the amount

- the reason

- the due date, if any

- the payment link or QR

- the expected UPI name

If a client wants to delay, they can delay in any payment flow. But a clear payment message removes the easy excuse of "I could not find the details" or "I was not sure this was you."

A cleaner way to request UPI payments

The end of person-to-person UPI collect requests is not a crisis for honest payments. It is a nudge toward better payment hygiene.

Instead of pushing a request into someone's UPI app, give them one clean place to pay you.

WithUPI helps you turn your UPI ID into a simple public payment page. It also gives you Requests for direct asks and group splits, so you can keep payment links, QR actions, notes, and statuses together.

That does not bypass UPI rules. It just makes the payer-initiated flow feel cleaner.