Best RuPay credit cards for UPI payments in India in 2026

A practical ranking of RuPay credit cards for UPI payments, cashback, rewards, travel points, and everyday scan-and-pay use in India.

Written by

WithUPI Team

Practical notes from the WithUPI team on trust, payment clarity, and better ways to present your UPI identity.

RuPay credit cards on UPI are worth considering for one reason: eligible QR payments can earn cashback, points, or travel rewards.

The trick is choosing the right card. Some cards reward only one app. Some cap cashback quickly. Some are excellent only if you already spend inside a specific ecosystem.

One important note before we start: credit card rewards change fast. Banks can change reward rates, merchant exclusions, caps, fees, and eligibility rules. Always check the current card page and terms before applying or spending.

Quick answer

If you want the short version:

- Best overall for UPI cashback: Kiwi RuPay Credit Card via Kiwi

- Best simple no-fee cashback card: Axis Bank super.money RuPay Credit Card

- Best for travel rewards on UPI: Scapia Federal RuPay Credit Card

- Best Tata ecosystem card: Tata Neu Infinity HDFC Bank Credit Card

- Best PhonePe ecosystem card: PhonePe HDFC Bank Ultimo Credit Card

- Best bank-issued virtual UPI card: HDFC Bank UPI RuPay Credit Card

- Best secured beginner card: IDFC FIRST EA₹N RuPay Credit Card

The top 10 RuPay credit cards for UPI payments right now

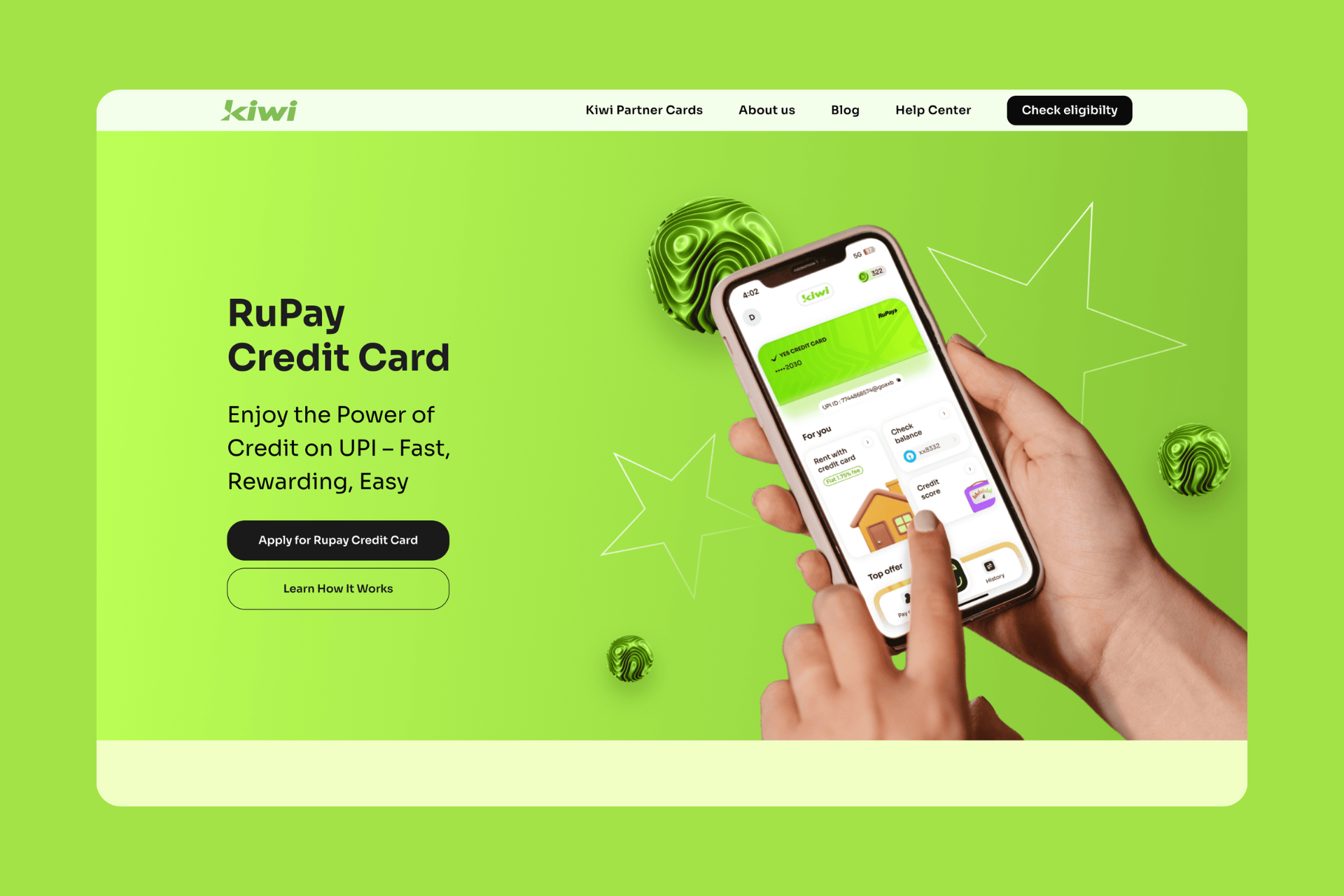

1. Kiwi RuPay Credit Card via Kiwi

Official website: Kiwi

Kiwi is the strongest pick if you want direct cashback on UPI. The card is built around scan-and-pay credit usage, so UPI is the main event rather than a side feature. Cashback goes directly to the bank account, which makes it easier to value than points or coins. Pick Kiwi if most of your eligible UPI payments happen at merchant QRs and you want the cleanest cashback setup.

Key rewards and terms:

- 1.5% flat cashback on everyday UPI payments

- paid Neon membership can raise rewards up to 5% cashback on UPI payments after spend milestones

- base setup is marketed as lifetime free

- highest rates depend on Kiwi's membership and milestone structure

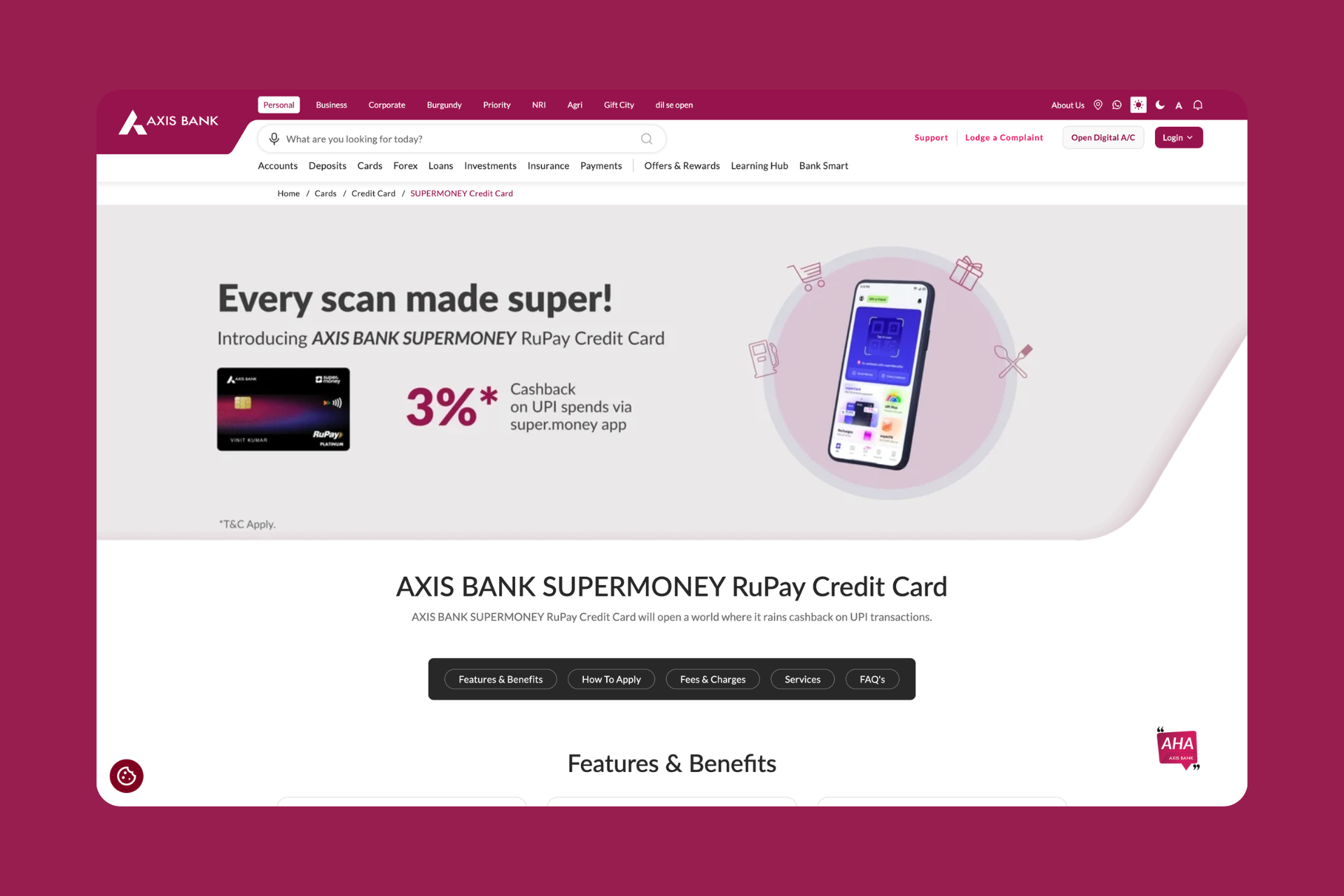

2. Axis Bank super.money RuPay Credit Card

Official website: Axis Bank super.money RuPay Credit Card

Axis Bank super.money is the best no-fee UPI cashback card if you are willing to use the super.money app. The 3% rate is strong, simple, and easy to beat only if you pay for a richer membership elsewhere. The ₹500 statement-cycle cap makes it ideal for moderate everyday QR spending, not unlimited heavy usage. Pick it if you want meaningful UPI cashback without a joining fee, annual fee, or subscription.

Key rewards and terms:

- 3% cashback on UPI transactions done via the super.money app

- 1% cashback on all other eligible spends

- cashback capped at ₹500 per statement cycle

- no joining or annual fee on the official card page

- restricted merchant categories do not earn cashback

3. Scapia Federal RuPay Credit Card

Official website: Federal Bank Scapia Credit Card

Scapia is the travel rewards pick. It is not the card to choose if you want cash in your bank account, but it is excellent if you already redeem rewards for trips. The card gives strong rewards on eligible UPI spends above ₹500, so it works better for meaningful purchases than tiny snack payments. Pick Scapia when your regular UPI spends can realistically turn into travel value through Scapia Coins.

Key rewards and terms:

- 5% reward on eligible UPI, online, and offline spends of ₹500 or more

- Scapia Pay says UPI payments above ₹500 made through Scapia Pay with a Scapia co-branded RuPay credit card earn 5% rewards as Scapia Coins

- 5 Scapia Coins equal ₹1 toward travel

- rewards are travel value, not direct cashback

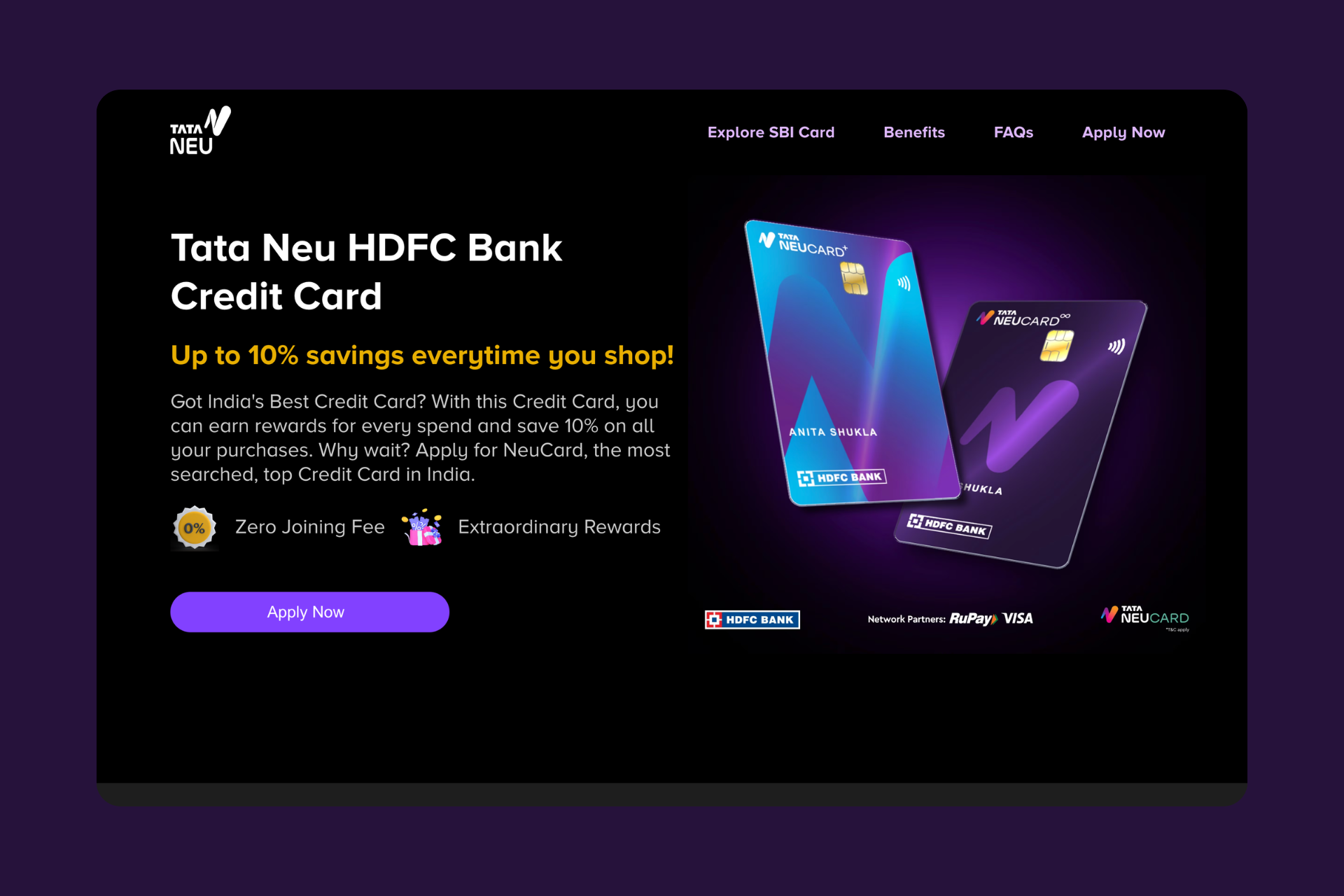

4. Tata Neu Infinity HDFC Bank Credit Card

Official website: Tata Neu Infinity HDFC Bank Credit Card

Tata Neu Infinity is the premium ecosystem card on this list. The UPI reward rate is useful, but the real reason to choose it is combined spending across Tata Neu, Bigbasket, Croma, Tata 1mg, Air India, IHCL, and Tata CLiQ. NeuCoins are also easier to value than many bank reward points because they generally map to ₹1 savings inside Tata Neu. Pick Infinity if your UPI payments and shopping already sit inside the Tata ecosystem.

Key rewards and terms:

- 1.5% back as NeuCoins on UPI spends

- UPI rewards capped at 500 NeuCoins per calendar month

- 5% back as NeuCoins on eligible spends on Tata Neu and partner Tata brands

- best value is inside the Tata ecosystem

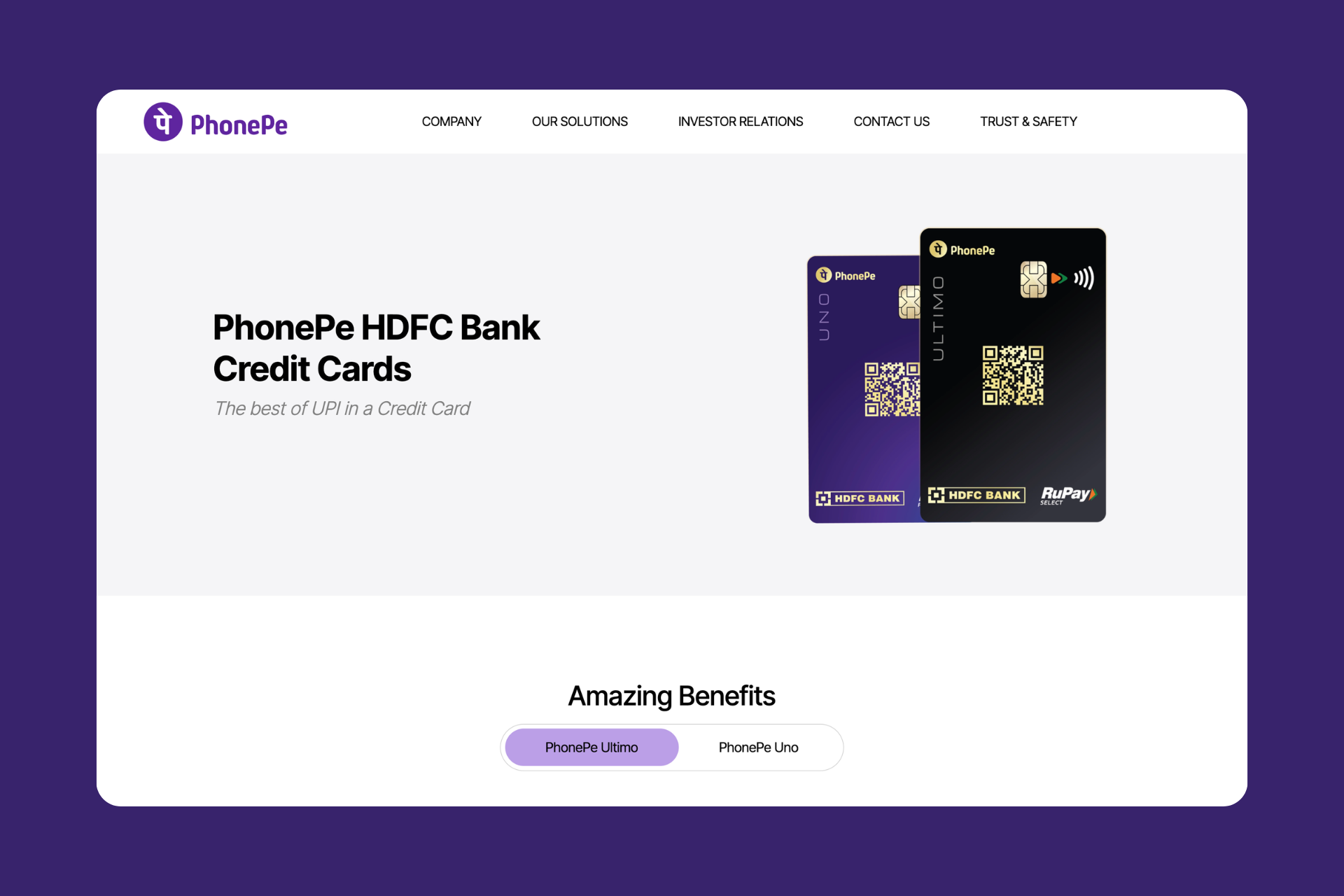

5. PhonePe HDFC Bank Ultimo Credit Card

Official website: PhonePe HDFC Bank Ultimo Credit Card

PhonePe Ultimo is strongest when PhonePe is more than your QR scanner. The 1% Scan & Pay reward is useful, but the upside comes from bills, recharges, travel, PhonePe PINCODE, and selected online brands. If you only scan merchant QRs, simpler cashback cards are easier. Pick Ultimo if your monthly PhonePe activity already overlaps with the 10% and 5% reward categories.

Key rewards and terms:

- 10% reward points on select PhonePe categories

- 5% reward points on select online brands

- 1% reward points on all Scan & Pay spends

- 1% Scan & Pay reward capped at 500 reward points per calendar month

- reward points can be redeemed against statement balance on request

6. HDFC Bank UPI RuPay Credit Card

Official website: HDFC Bank UPI RuPay Credit Card

HDFC Bank UPI RuPay Credit Card is the clean bank-issued option. It is virtual-only and built specifically for UPI, which makes it practical for existing HDFC Bank customers who do not want to shift their payments into a fintech app. The reward structure works best when your UPI spends are groceries, utilities, dining, or PayZapp-heavy. Pick it if you want a straightforward HDFC card for digital payments, not the highest possible cashback rate.

Key rewards and terms:

- 3% CashPoints on groceries, supermarket, dining, and PayZapp transactions

- 2% CashPoints on utility spends

- 1% CashPoints on other eligible spends

- benefits apply to both UPI and regular credit card spends, with category caps

- available as a virtual-only card for existing HDFC Bank customers

7. Tata Neu Plus HDFC Bank Credit Card

Official website: Tata Neu Plus HDFC Bank Credit Card

Tata Neu Plus is the lower-commitment Tata card. It gives a lower UPI reward rate than Infinity, but it still works for households that shop across Tata brands without needing the higher tier. The card is easier to justify when your Tata spends are steady but not large enough to chase premium value. Pick Neu Plus if you want NeuCoins from everyday UPI and Tata spends without stepping up to Infinity.

Key rewards and terms:

- 1% back as NeuCoins on UPI spends

- UPI rewards capped at 500 NeuCoins per calendar month

- 2% back as NeuCoins on eligible non-EMI spends on Tata Neu and partner Tata brands

- best redemption value is tied to Tata Neu

8. PhonePe HDFC Bank Uno Credit Card

Official website: PhonePe HDFC Bank Uno Credit Card

PhonePe Uno is the lighter PhonePe card. It keeps 1% rewards on Scan & Pay spends, but cuts down the broader category upside compared with Ultimo. That makes it a better fit for routine QR payments and occasional PhonePe spends, not full monthly optimization. Pick Uno if Ultimo's higher reward categories do not match your real spending.

Key rewards and terms:

- 2% reward points on select PhonePe categories

- 1% reward points on select online brands

- 1% reward points on all Scan & Pay spends

- monthly caps apply

- many categories are excluded

9. IDFC FIRST EA₹N RuPay Credit Card

Official website: IDFC FIRST EA₹N Credit Card

IDFC FIRST EA₹N is the starter card. It is secured by a fixed deposit, so it solves a different problem from the cashback-heavy cards above: access. The UPI cashback is lower, but the card helps students, new earners, and thin-file users build credit history. Pick EA₹N when getting a RuPay credit card matters more than maximizing reward percentage.

Key rewards and terms:

- up to 1% cashback on UPI spends via the IDFC FIRST Bank mobile app

- 0.5% cashback on other UPI app transactions

- requires a fixed deposit

- useful for building credit history

10. SimplySAVE UPI SBI Card

Official website: SimplySAVE UPI SBI Card

SimplySAVE UPI SBI Card is the familiar issuer pick. It does not have the sharpest UPI cashback pitch, but it gives a straightforward RuPay UPI card from SBI Card with accelerated rewards in common everyday categories. The card makes most sense when you prefer a traditional issuer and reward points over fintech-led cashback experiments. Pick it for grocery, department store, dining, and movie spending, not maximum UPI cashback.

Key rewards and terms:

- card can be linked to any UPI app

- interest-free credit period on everyday needs

- 10 reward points per ₹150 spent on dining, movies, departmental stores, and grocery spends

- 1 reward point per ₹150 on other spends

- rewards are points, not direct cashback

Which card should you choose?

Choose Kiwi if you want the cleanest UPI cashback card and are happy using Kiwi for scan-and-pay.

Choose Axis Bank super.money if you want strong no-fee cashback and your monthly UPI rewards will stay within the ₹500 cap.

Choose Scapia if travel redemption is useful to you and most of your eligible UPI payments are above ₹500.

Choose Tata Neu Infinity if Tata brands already take a large share of your monthly spending.

Choose PhonePe Ultimo if PhonePe handles your bills, recharges, travel, online spends, and QR payments in one place.

Choose HDFC Bank UPI RuPay Credit Card if you already bank with HDFC and want a simple virtual UPI credit card.

Choose Tata Neu Plus if you want Tata Neu rewards but your spending does not justify the Infinity tier.

Choose PhonePe Uno if you use PhonePe regularly but not enough to benefit from Ultimo's higher categories.

Choose IDFC FIRST EA₹N if you need a secured card to start building credit.

Choose SimplySAVE UPI SBI Card if you prefer SBI Card and want basic reward points on familiar daily categories.

The best card is the one that rewards payments you already make. If you need to change your spending just to justify a card, skip it.

How RuPay credit card on UPI works

NPCI's RuPay Credit Card on UPI FAQ says only RuPay credit cards can currently be linked on UPI.

The big rule is simple: RuPay credit cards on UPI are for merchant payments. NPCI says person-to-merchant transactions are allowed from the linked credit card, while person-to-person payments are not allowed.

That means you can use the card at eligible merchant QRs, but you cannot use it to send money to friends or family. You also cannot receive money on the credit card.

Why RuPay credit card on UPI sometimes fails

This is one of the most common frustrations.

You link the card. You scan a QR. Then the app does not show the credit card as a payment option, or the payment fails.

That can happen because:

- the QR belongs to a person, not an eligible merchant

- the merchant has disabled credit-card UPI acceptance

- the transaction falls into a restricted category

- the UPI app does not support that card properly

- your bank has a limit or risk check

- your card is newly linked and has a temporary lower limit

- the merchant category does not earn rewards even if the payment works

NPCI's RuPay credit card on UPI page specifically warns users not to use this feature for categories like person-to-person payments, digital account opening, lending platforms, cash withdrawal, card-to-card payments, IPO, foreign inward remittances, mutual funds, and other restricted categories.

So if your RuPay credit card on UPI does not work at a local shop, it does not always mean your card is bad. The merchant setup is often the reason.

RuPay credit card on UPI vs normal bank UPI

Use normal bank UPI when:

- you are paying friends or family

- the merchant does not accept credit-card UPI

- you do not want to use credit

- you want the simplest possible payment flow

- you are close to your credit card due date and do not want to add more spend

Use RuPay credit card on UPI when:

- the merchant accepts it

- you want rewards or cashback

- you can repay the bill in full

- the transaction category is eligible

- the reward value is worth the extra credit-card tracking

The golden rule is simple: never spend more just to earn rewards.

UPI credit card rewards are useful only when they sit on top of payments you were already going to make.

What recipients should know

If you collect UPI payments as a freelancer, creator, tutor, or small business owner, RuPay credit card on UPI changes one thing: some payers now expect a merchant-style QR or payment flow that supports their preferred credit card.

That will not always work. Personal UPI IDs are different from eligible merchant QRs, and credit-card UPI is not available for person-to-person payments.

The practical move is to make your payment details clear:

- one correct UPI ID

- one QR code

- one payment link

- the name the payer should see

- a note if credit-card UPI is not supported for your setup

A clean payment page helps here because it gives the payer one place to check the payment destination before opening their UPI app. WithUPI is one simple way to create that page, but the broader point is the same no matter what you use: reduce confusion before the payment starts.